Realpolitik

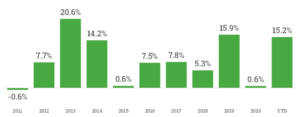

The Value Fund was up +1.3% in Q3 and is up +15.2% year-to-date (YTD) net of fees and expenses. The strengthening US dollar increased our returns by approximately 2.0% in the quarter but has lowered them by -0.5% YTD. As of September 30, the S&P/TSX Total Return Index was up +17.5% and the S&P500 Total Return Index ($CAD) +15.3%.

Our best performing stock in Q3 was our investment in Alphabet (GOOG/GOOGL) +6.3%. The search juggernaut continues to deliver impressive revenue growth and record profits. Despite the stock’s rise, we believe it is still modestly undervalued. We have owned GOOG since 2018 and given our view of their long-term prospects, hope to remain a shareholder for years to come. It remains our second-largest position.

Pfizer (PFE) +9.8% was our second-best contributor for the quarter. Purchased in March 2020 along with our investment in Merck (MRK), they both offered modest valuations, decent dividend yields, and we figured that these companies might just save the world from COVID-19. Pfizer (and humankind) hit the jackpot with their mRNA vaccine which they cannot manufacture fast enough. Pfizer’s vaccine sales should exceed $50 billion next year, and we are up about +44% on our investment as a result. Merck’s vaccine candidate was a disappointment, but their COVID-19 treatment drug (molnupiravir) looks to be both safe and effective. FDA emergency-use authorization should be forthcoming. We are only up +11% on our investment in Merck but given the quality of their balance sheet and cash flow generation from their powerhouse cancer drug (Keytruda), we continue to like the name.

Rounding out the top three contributors for the quarter was CBOE Global Markets (CBOE) +4.0%. CBOE operates the largest U.S. options exchange and several North American and European stock exchanges. Our position in CBOE is up over 50% since we purchased it in late 2020. The stock is about fairly valued in our opinion, but part of our investment thesis is that CBOE would be an attractive acquisition target for the larger exchange players like ICE, Nasdaq or CME. Until we find a more attractive opportunity, we prefer to hold the stock to preserve that optionality.

Our largest detractor during the quarter was Visa (V) -4.7%. The stock is more than fully valued at present but given its long-term growth rate and our cost basis of $79.38, we have no desire to part with it. Visa is a compounder and one of the best business models we have come across.

Intel (INTC) -5.1% was our second-worst performer for the quarter. Just this past week the company reported decent Q3 results but lowered its long-term margin guidance and the stock sold off further. We are about flat on our investment as of writing. We like the strategic direction of the firm under new CEO Pat Gelsinger and believe that they have a credible shot at regaining process leadership from TSMC. But the turnaround is going to take years given the missteps of the past. More positively, our view of the strategic importance of Intel’s manufacturing capacity to the West is coming into greater focus due to China’s increasingly frequent military sorties around Taiwan.

“No Chinese leader has ever abandoned the insistence on ultimate unification [of Taiwan] or can be expected to do so. No foreseeable American leader will jettison the American conviction that this process should be peaceful or alter the American view on the subject”.

Henry Kissinger, On China (1)

The US and China have managed the Taiwan issue for decades via deliberate ambiguity. Given recent events in Hong Kong and China’s increasing assertiveness, we believe that China will eventually reel in its ‘renegade province’. If that happens, the West’s supply chain for some 90% of the world’s most advanced semiconductors will be controlled by China.

In recent years, the US has restricted the sale of high-end semiconductor equipment to China. A China-controlled Taiwan is unlikely to forget. No wonder Europe and the US are starting to subsidize Intel’s capital investments in new fabs in their backyards. The West needs Intel to succeed and we believe that they ultimately will. But our investment is likely to take some time to play out.

We added to a few positions and trimmed a few others during the quarter based on valuations on offer. But overall, it was a quiet quarter for the portfolio with no major changes. With the portfolio up +15.2% YTD we are in a good position heading into the final quarter of 2021. Earnings season is now in full swing, and we are looking for opportunities. That said, are mindful of risk given the market’s overall valuation.

(1) Kissinger, Henry. On China. Penguin, 2011, p. 272.

Portfolio “Look Through”

Quantifying the quality of our portfolio via our look-through analysis in Scorecard #34 proved to be popular with clients. We received very positive feedback and as a result, will be giving this analysis a permanent place in our Annual Reports going forward.

Source: Greenskeeper Asset Management / Bloomberg / S&P Capital IQ. Return on Equity, Gross Margin, Operating Margin, Cash Conversion and Free Cash Flow Yield are the weighted mean of the underlying companies invested in by the Greenskeeper Value Fund and the mean for the S&P 500 Index. The S&P 500 Index figures exclude financial stocks except for ROE which includes all sectors. Interest coverage figures are median and exclude financial stocks. Ratios are based on last reported fiscal year accounts as at the respective dates and as defined by S&P Capital IQ. Cash Conversion compares Free Cash Flow with Net Income. Free Cash Flow Yield for the S&P500 uses the period-end median. *2021 figures as of June 30.

Rule of Law

It isn’t often that we disagree with Charlie Munger, but his penchant for investing in China leaves us scratching our heads. The Value Fund does not and will not invest in companies domiciled in China, South America, Russia, India and many other places. Our stance isn’t ideological. It is pragmatic based on our assessment of the risks involved and warrants some elaboration.

China

After the disaster of Chairman Mao’s Great Leap Forward, economic reforms were introduced by Deng Xiaoping in the 1970s and embraced by his successors. ‘Socialism with Chinese characteristics’ ushered in an era of freer markets, foreign investment and the unleashing of the talents of the Chinese people. China’s economic miracle of the past 40 years has lifted hundreds of millions of its citizens out of poverty and improved the life of the average Chinese citizen. China’s rise is befitting for this ancient and great civilization.

China’s economic rise will likely continue. So why not invest in companies that are at the center of that growth? In our opinion, the risks involved vastly outweigh the potential rewards.

First, China prohibits foreign investment in many sensitive industries. To circumvent these restrictions, many Chinese companies created offshore variable-interest entities (VIEs) that have a contractual right to the profits of the underlying Chinese company. It may surprise you to learn that when someone purchases a Chinese ‘stock’ on a North American exchange (e.g., BABA, DIDI), they are in fact purchasing a claim on the VIE. Whether or not this arrangement is legal under Chinese law remains unclear.

Even if this structure is legal, the reality is that if a foreign investor’s contractual rights are trampled upon, they have little recourse via China’s courts. Laws are deliberately vague and the Chinese judiciary hardly independent. The Chinese Communist Party (CCP) is the law in China. Does anyone doubt that the CCP can confiscate assets with the stroke of a pen? The recent crackdown on Chinese tech titans should be treated as a warning by foreign investors. If the state is willing to squeeze its own citizens and corporate champions, do you think that foreign investors are likely to be treated more favourably? The power and supremacy of the CCP is paramount and the CCP will do what is in China’s national interests. I have no desire to invest our capital under these circumstances.

South America

The prevailing attitude towards foreign investors that exists in many South American countries was nicely summed up by President Bolsonaro of Brazil earlier this year. After firing the CEO of state-controlled oil giant Petrobras (on Facebook and without consulting the board), and replacing him with an army general, he came out with this beauty: “Is the petroleum ours, or does it belong to a small group of investors?”

So, the Brazilian state is happy to take capital from international investors, and then ignore their rights whenever it is politically convenient to do so.

Only a century ago, Argentina was one of the richest countries in the world. Bad policy choices, malfeasance and ineptitude have led to multiple bouts of hyperinflation and sovereign debt defaults since that golden era. As a result, Argentina has been kept woefully short of its true potential and foreign investors repeatedly burned.

The Rest

Despite being a democracy, India’s nationalist Modi government has no qualms abusing state power for political reasons and showing hostility towards foreign investment. Russia, … well hopefully you understand the risks of investing in a country where the president for life is the law.

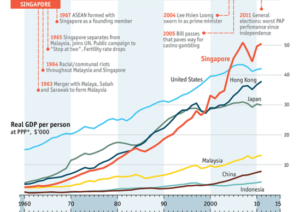

It doesn’t have to be this way. A few developing nations have been able to get it right. Singapore, a city state that started out as an impoverished swamp with few natural resources grew into a developed nation with the highest GDP per capita in Southeast Asia. How did they do it? By building infrastructure, making sound policy choices, and courting foreign investment.

In the words of Singapore’s founding father Lee Kwan Yew:

“If I have to choose one word to explain why Singapore succeeded, it is ‘confidence’. This was what made foreign investors site their factories and refineries here… The foundations for our financial center were the rule of law, an independent judiciary, and a stable, competent and honest government that pursued sound macroeconomic policies, with budget surpluses almost every year”. (2)

“An astonishing record”, The Economist. 22 Mar. 2015.

(2) Lee, Kuan Yew. From Third World to First: The Singapore Story, 1965-2000: Singapore and the Asian Economic Boom. HarperCollins, 2000. This is the second volume of a two-volume memoir written by Mr. Lee. Highly recommend reading along with the first volume: Lee, Kuan Yew. The Singapore Story: Memoirs of Lee Kuan Yew. Prentice-Hall, 1998.

Singapore’s success is simple but not easy. Millions of people in less-developed nations would live better lives if these principles were embraced and properly implemented. In the meantime, we will keep our capital invested in countries that follow Singapore’s simple principles, especially respect for the rule of law. We prefer to compete in contests where the rules are laid out in advance and enforced by impartial referees.

Western-domiciled companies are a large enough hunting ground for investment candidates at GreensKeeper. While we may miss out on a few opportunities in more exotic locations, preservation of capital and risk mitigation takes precedence. Besides, while most of the world’s great companies are multinationals based in the United States, they sell their goods and services worldwide. We still get exposure to faster-growing markets but in a more prudent way.

On the Lighter Side

This recent video clip on CNBC made us laugh. It is worth a minute of your time and reinforces our view of stock market TV. While BNN Bloomberg and CNBC can be insightful at times, much of their programming is pure entertainment. We prefer to spend our time reading financial statements and management transcripts instead of watching market “experts”.

In the current age, we are all inundated with too much information. Without effective filters and mental models, useful signals are lost in the noise. Our most valuable commodity is our time. Spend it wisely.

We look forward to providing you with our Annual Report early in the new year. Until then, thank you for the trust and confidence you have placed in GreensKeeper by investing with us. We are working hard to grow your capital alongside our own.

Michael P. McCloskey

President, Founder &

Chief Investment Officer