Momentum

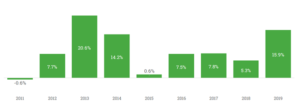

The Value Fund returned +15.9% in 2019 net of fees and expenses and has returned +9.5% net since inception on November 1, 2011. This past year was our eighth consecutive year of positive returns.

The panicked selloff of Q4 2018 now seems like a distant memory as investor mood quickly swung to euphoria last year driving equity markets higher across the globe. Given our conservative bent and willingness to hold cash when stocks are expensive, we trailed our benchmarks in 2019. The S&P/TSX Total Return Index finished up +22.9% and the S&P500 Total Return Index, measured in Canadian dollars (the Value Fund’s reporting currency) was up +25.1% for the year.

We tend to outperform in ugly markets as we did in 2018. High quality companies that are undervalued tend to hold up better under stress. Risk management and preserving capital is a cornerstone of our investment framework at GreensKeeper. As American race car driver Rick Mears so aptly put it, “to finish first, you must first finish”. Our goal is to prudently compound your capital (and ours) and avoid costly pile ups that set so many investors back. So far, so good.

Given our significant U.S. stock holdings, the 5% appreciation of the Canadian dollar in 2019 lowered our returns by approximately the same amount. The loonie was the best performing major currency in the world last year versus the U.S. dollar. We view these swings as entirely unpredictable and largely noise. Exchange rate impacts on portfolio returns tend to be a wash over the long term. A more detailed explanation of our view on currency hedging (and our bias for not doing so) can be found here.

Market Outlook

So what will equity markets do in 2020? I was asked that exact question by a group of professional money managers in Toronto recently. My response left them wanting. I don’t have any idea and firmly believe that neither does anyone else. Those that profess to know like the daily pundits on CNBC or BNN Bloomberg TV may be entertaining to listen to, but don’t mistake their commentary for wisdom. Making investment decisions based on market projections has proven time and time again to be a fool’s errand.

It shouldn’t surprise you that our investment heroes (Munger, Buffett, Graham) share our view. As bottom-up value investors we simply look for great businesses that are selling cheap regardless of market conditions. When we find one that meets our criteria, we pull the trigger. In fact, selloffs tend to be fertile hunting ground for us. When investors panic, opportunity presents itself as it did for the Value Fund portfolio in Q4 2018.

Portfolio Review

Our two biggest contributors to the portfolio in 2019 were our investments in Apple +58.8% (AAPL) and Facebook +56.6% (FB), both of which were purchased during the Q4 2018 selloff. Those two stocks contributed about 4.8% to our 2019 returns. Just a few meaningful and timely decisions can make a big difference to portfolio returns.

When we were buying Apple, investors worried that the company had reached peak iPhone volumes and sales to China were also declining rapidly due to the US/China trade war. Fast forward to today and what has changed? Consensus 2020 earnings for the company is currently $13.12 per share. This is lower than the $13.43 consensus at the time of our purchase. In other words, Apple’s business isn’t materially different today. What has changed, to a remarkable degree, is investor sentiment about the stock.

With an average purchase price of $155.30, we bought the stock for 11x earnings plus cash. In other words, absent a material change in Apple’s business, this was not a risky investment. At the current share price of $317.70, investors are now prepared to pay 22x earnings for the same company only one year later. We fully exited our position in Apple late in the year as we believe the stock is more than fully-valued at current prices.

Apple is a strange case study. We made a handsome return on one of the most well-followed companies on the planet in about 10 months. Since selling the stock it has continued its upward rise unabated. So perhaps we sold too early as value investors trying to manage risk often do. Or perhaps investors are getting a little carried away again, just in the opposite direction. As a consolation, we still have plenty of exposure to the company through our shareholdings in Berkshire Hathaway (BRK.A/BRK.B). Assuming the Oracle hasn’t sold any shares, Berkshire holds about $79 billion worth of Apple stock.

We wrote about our investment thesis for Facebook at length in last year’s annual report. The company is still the favourite whipping boy of regulators and politicians. But in a US campaign year, where do your think that politicians are spending much of their campaign dollars? The number of users on the company’s platforms (Facebook, Instagram, WhatsApp) continues to grow. Profits are massive and the cash keeps piling up. At our average cost of $141.29 per share we are currently up 57% on our investment but unlike Apple, we haven’t sold a share.

We believe that Facebook has the potential to be a compounder – a company that increases its intrinsic value for many years to come. The Instagram app is only starting to be monetized and from what we can tell, WhatsApp doesn’t generate any meaningful revenue despite billions of active users.

Our bet is that over time the company will find a way to monetize these users and that earnings will continue to increase at a handsome pace.

Our only beef with Facebook is management’s questionable capital allocation decisions. We don’t mind them investing in people, servers and data centers to service their customers and grow the business. But with $52 billion of cash on the balance sheet and no debt, we just wish they would repurchase their stock more aggressively, especially when it’s cheap.

Our next largest contributors for the year were our credit card network investments: Visa +42.4% (V) and American Express +30.6% (AXP). These high-quality compounders continue to grow earnings and should thrive for many, many years to come. Accordingly, absent a material disruption to their business or an obviously superior investment alternative, we view these positions as core holdings.

Rounding out the top 5 for 2019 was our investment in S&P Global +60.7% (SPGI). The company’s main business is its credit rating agency – Standard & Poor’s. Oligopolies tend to be great businesses and S&P and Moody’s are the dominant firms providing credit rating services to issuers worldwide. Pricing power combined with a capital-light business makes them free-cash-flow machines with very high returns on capital. The Federal Reserve’s recent decision to lower interest rates also encourages debt issuance which provides a helpful tailwind for the company. We believe that the formation of debt capital markets in new geographies (e.g. Asia) should provide future growth opportunities for S&P Global for decades to come.

While it is still early days for our stock positions in the US health insurers – UnitedHealth Group (UNH) and Anthem (ANTM), so far so good. The stocks are up 18.6% and 28.6% respectively since our purchases in Q4. It seems that the market is coming around to share our view that Medicare for All is unlikely to happen.

Given the overall bullish markets, we only had two stocks that were in the red for the year. Tapestry -19.7% (TPR) – formerly known as Coach – lowered our returns by (0.3%) in 2019. We fully exited the stock in Q3. Tapestry was a disappointing investment for us. The reason? We simply got this one wrong. It looked cheap when we bought it, but the company was overly promotional and did some lasting damage to the brand. Add in growing competition from Michael Kors and the rise of fake merchandise via ecommerce and we ended up with a poor result.

Brands and retail in general are both changing rapidly due to technology making it easier for new competitors to reach consumers directly. Lesson learned.

We also fully exited our investment in Sanofi -8.1% (SNY) during the year. Sanofi was a small legacy investment for the Value Fund. We were originally attracted to the company given its exposure to the diabetes market – a large and growing segment. Diabetes care is largely an oligopoly comprised of Novo Nordisk (NVO), Eli Lilly (LLY) and Sanofi. While we sold our position in Sanofi at a profit, it was a mediocre investment. We still like the diabetes sector and have plenty of exposure via our stake in market-leader Novo Nordisk (4.7% weighting).

During the year we also profitably exited our positions in Coca-Cola European Partners (CCEP) and McKesson (MCK) as both stocks reached our target prices. We also fully exited our position in AT&T (T) but for different reasons. The stock remains cheap but has a balance sheet that gives us heartburn. Given our view that we are late in the economic cycle, we believe there are better (and safer) places to invest at the present time.

Overall 2019 was a solid year for the Value Fund. We finished the year with a net cash position of 17.3% and unrealized gains on our equity investments of approximately $8.2 million on a $34.8 million portfolio. Additional portfolio disclosures including performance statistics can be found on the pages immediately following this letter. Once KPMG completes its audit of the Value Fund’s Financial Statements in March, we will provide clients with a more detailed snapshot of the entire portfolio at year end.

The Value Fund’s top 10 holdings, representing over 63% of the portfolio at year end, were as follows:

*As at December 31, 2019. The Value Fund’s holdings are subject

to change and are not recommendations to buy or sell any security

2020 and Beyond

The past year was a year of record growth for the Value Fund and our Managed Account portfolios. To fuel our next leg of growth, we launched the Value Fund on the Fundserv platform in November. As a result, selected investment advisers can now offer Value Fund units to their clients directly through their brokerages.

Earlier this month, we also announced an exciting addition to the firm’s leadership team. After successfully completing the requisite coursework and being duly licensed by the Ontario Securities Commission, my brother James joined the firm as Senior Vice President – Sales. James brings over 15 years of sales experience with high-net-worth individuals to GreensKeeper and I am looking forward to continuing the firm’s growth with him by my side. James and I be in touch later this year regarding an investor meeting, but in the meantime please feel free to reach out to either of us with any questions.

Finally, I would like to take a moment to thank all our clients for the trust that you continue to place in us and for referring others to GreensKeeper. We will continue working hard to grow your capital alongside our own.

Michael P. McCloskey

President, Founder &

Chief Investment Officer